How many people do you know own a diamond in some form? Whether bought as a mark of success, passed down through generations, or given as symbols of love, marriage, or commitment, diamonds have long represented both status and sentiment. For more than a century, natural diamonds have traded on a sense of rarity and therefore, a hefty price tag; yet, this has been sustained more by perception than fact.

This illusion is beginning to crack. Lab-grown diamonds, identical visually and chemically, can be produced in days and sold at a fraction of the price. In New York’s Diamond District, loose lab-grown stones now sell for US $135 to $175 per carat, while natural equivalents cost roughly ten to twenty times more, depending on size, cut, colour and clarity. This dramatic price gap has cemented lab-grown diamonds in the market, positioning them as serious competitors to natural stones and reshaping not only how diamonds are bought but what they symbolise and who can access them.

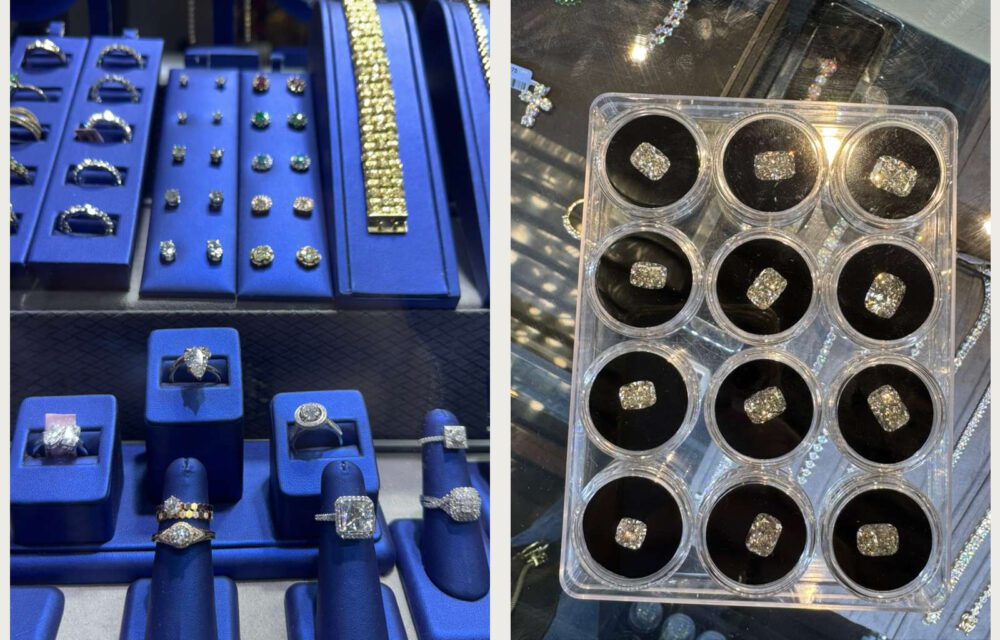

(Pictured Left to Right. Mined Diamond Assorted Jewellery, Lab-grown Loose Diamond Stones. New Yorks’ Diamond District, 2025 | in.Parallel images)

(Pictured Left to Right. Mined Diamond Assorted Jewellery, Lab-grown Loose Diamond Stones. New Yorks’ Diamond District, 2025 | in.Parallel images)

Now consumers face the uncomfortable question. If the financial value has collapsed, are we still willing to pay a premium purely for the meaning we attach to the stone? And if diamonds are suddenly accessible to everyone, does the symbol gain power or lose it?

The idea that diamonds are valuable because they are rare is one of modern luxury’s most successful fictions. It seems intuitive, since stones forged over millions of years beneath the earth’s surface should be scarce. Yet, their rarity was never geological. It was engineered through economic control over supply and one of the most successful marketing efforts of the twentieth century.

The system began in 1888 when British imperialist Cecil Rhodes consolidated South Africa’s mines into De Beers Consolidated Mines. This merger laid the foundation for a corporation that would dominate the global diamond trade for the next century. By the mid-twentieth century, under the Oppenheimer family, De Beers controlled nearly 90% of the world’s rough diamonds. Preserving the illusion of scarcity, surplus stones were locked in London vaults and released in tightly managed quotas (1).

Until the 1950s, diamonds had little to do with love. Signalling rank and status, they were worn in abundance on crowns and jewellery by royalty and the aristocracy. Instead, engagement rings worn by the wider public were often set with coloured gemstones, since few could justify the cost of diamonds. In fact, in 1939, only about 10% of American brides received a diamond ring (2).

Facing stagnant sales after the Depression, and with lavish displays of wealth falling out of favour among the old elite, De Beers needed a new audience. They turned to Philadelphia marketing agency N. W. Ayer and Son with a simple brief: make people want diamonds again. The agency leaned on the geological story to sell emotion, and in 1947 coined “A Diamond Is Forever.” These four words transformed a shiny mineral into the ultimate symbol of eternal love, equating geological endurance with the emotional commitment expected of a lifelong partnership.

(Gentlemen Prefer Blondes Trailer, 1953)

(Gentlemen Prefer Blondes Trailer, 1953)

Diamonds soon flashed on the hands of Hollywood’s leading ladies and appeared in films from Gentlemen Prefer Blondes in 1953 to Diamonds Are Forever in 1971. The slogan had moved beyond advertising and embedded itself in the cultural zeitgeist as the ultimate symbol of status, glamour, the carefully engineered belief that love should be sealed with a stone. The results were staggering; De Beers’ US sales leapt from $23 million in 1939 to its peak of more than $2 billion by 1979 (3).

Meanwhile, in 1954, scientists at General Electric achieved what De Beers had long implied only nature could do, they manufactured a diamond. The first stones were industrial grade, suitable for tools rather than jewellery, yet the breakthrough quietly set the groundwork for a shift in what “real” would come to mean in the diamond trade.

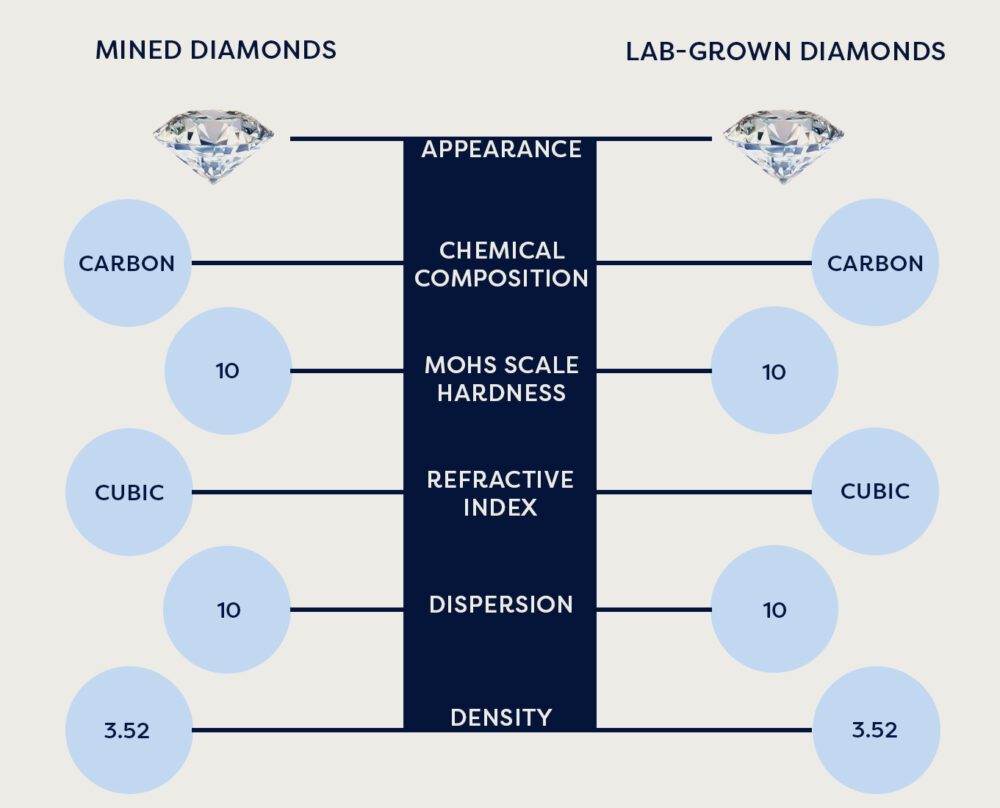

Natural diamonds form when carbon is exposed to extreme heat and pressure deep within the earth over millions of years, then carried upwards by rare volcanic events. Since the 2010s, advances in technology have allowed two lab-grown techniques to mimic these conditions and dominate production across both jewellery and industrial diamonds. High Pressure High Temperature (HPHT) compresses carbon into crystal form, and Chemical Vapour Deposition (CVD) grows diamonds atom by atom in a plasma chamber. Both produce stones that are chemically and optically identical to mined diamonds, and even expert gemologists require specialised instruments to tell them apart.

(Physical Properties of Mined vs Lab-Grown Diamonds taken from Queensmith | in.Parallel Graphic)

(Physical Properties of Mined vs Lab-Grown Diamonds taken from Queensmith | in.Parallel Graphic)

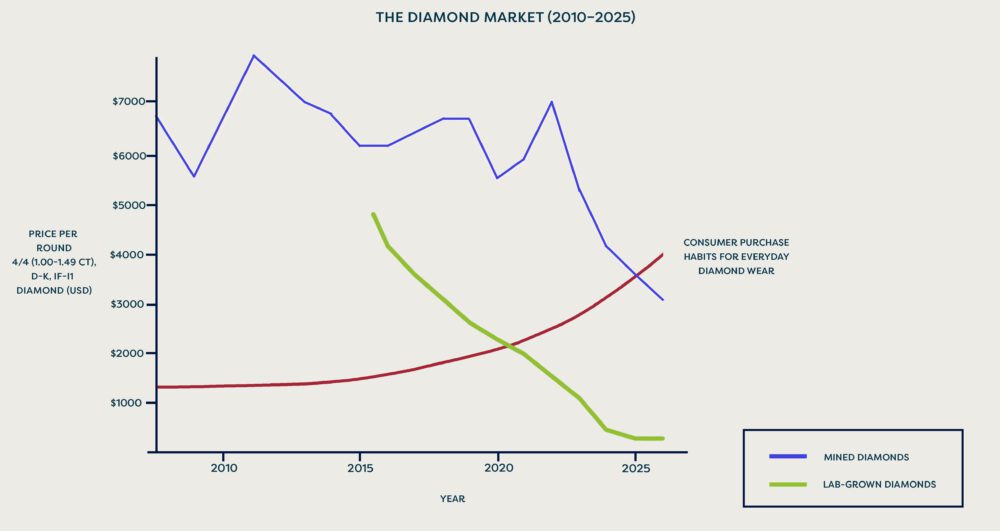

The result has been a market correction that even De Beers has not escaped. Data from Tenoris, a diamond analytics firm, stated a one-carat natural diamond fell from a peak of $6,819 in May 2022 to $4,997 by December 2024; a drop of nearly 27%, driven largely by the rise of lab stones (4). It’s been reported that lab-grown diamonds now make up more than half of all engagement ring centre stones sold in the US (5), and in New York, some dealers say lab-grown stones account for up to 90% of their sales. This is driven by “women wanting bigger stones and men wanting a price they can afford.”

While De Beers tried to compete in the lab-grown market with its 2018 venture Lightbox, the brand was shut down in 2024-25 as prices dropped below US $800 per carat and its fixed-price model collapsed under the surge of high-quality lab-grown supply (6). Additionally, Anglo American, DeBeers’ majority owner, wrote down the value of its diamond division by US $1.6 billion in 2023 and another US $2.9 billion in 20247. This decline paved the way for Anglo’s decision to put its 85% stake in DeBeers up for sale for US $5 billion in August 2025 (7), although analysts expect the final sale price to land closer to US $3-4 billion (8).

(A Shift in the Diamond Market. Data taken from Idex Diamond Prices | in.Parallel Graphic)

(A Shift in the Diamond Market. Data taken from Idex Diamond Prices | in.Parallel Graphic)

As the market recalibrates how it values diamonds, buyers are putting more weight on brand, precious metal and antique-stone appeal rather than the stone alone. Gold has reasserted itself as a dependable store of worth, with purity and weight driving value and price reaching record highs in 2024 and continuing to rise through 2025 and into 2026 (9).

(Pictures Left to Right: Graff shop window, Cartier storefront, Moussaieff shop window. New Bond Street, London | in.Parallel images)

(Pictures Left to Right: Graff shop window, Cartier storefront, Moussaieff shop window. New Bond Street, London | in.Parallel images)

Brand power has become a key source of stability, with value increasingly tied to the name on the box. As wider luxury sales slow, jewellery stands apart. Richemont’s maisons, from Cartier to Van Cleef & Arpels, grew 17% YOY and lifted the group’s overall sales by 10% in Q3 2025, (10) despite weakness in fashion and watches. LVMH, flat for two quarters, found its exception in Tiffany, which posted 2% organic growth (11) in Q3 2025 also driven by fine jewellery (12). These luxury brands hold their worth because their cultural capital endures. A Cartier Love bracelet will outperform an unbranded equivalent made from the same materials. The premium comes from reputation, not geology.

Antique stones offer a final exception. Their rarity is genuine, rooted in history rather than manufactured scarcity. Old mine and old European cuts have renewed appeal, helped by cultural signals such as Taylor Swift’s antique diamond engagement ring. “I see younger clients developing a deeper appreciation for antique stones and uniqueness. They’re gravitating towards pieces that are one-of-a-kind and rooted in history, which naturally leads them back to mined diamonds” says New York jewellery designer Stephanie Gottlieb. They are hand cut, each one slightly irregular, which gives them a uniqueness modern precision cannot replicate. In a market flooded with technically perfect lab-grown stones, their warmer tones and imperfect symmetry feel more human and more desirable. They also span a wide price range, which brings them within reach of a broader audience. These stones retain value because they are finite, crafted in a world before mass extraction, and they carry a romance neither lab-grown nor contemporary natural diamonds can match.

(Taylor Swift’s Old Mined Cut Engagement Ring)

(Taylor Swift’s Old Mined Cut Engagement Ring)

In recent decades, fine jewellery has shifted from milestone markers to everyday luxuries, seen in everything from classic studs and tennis bracelets to necklaces with diamond pendants, religious icons or playful charms. This evolution has also created space for contemporary designers offering different propositions.

(Pictured Left to Right. Arielle Ratner’s Diamond Floral Pendant, Stephanie Gottlieb’s Slider Bangle with Diamond Charms, Jessica McCormack’s Assorted Diamond Earrings & Ring, 2025)

(Pictured Left to Right. Arielle Ratner’s Diamond Floral Pendant, Stephanie Gottlieb’s Slider Bangle with Diamond Charms, Jessica McCormack’s Assorted Diamond Earrings & Ring, 2025)

Names like Jessica McCormack, Stephanie Gottlieb, Arielle Ratner, and Ming Jewellery pair sculptural, directional design with traditional high-jewellery craftsmanship. Their work centres on mined stones because their brands still rely on what natural diamonds signal, such as heirloom value, emotional significance, and cultural prestige. “Natural diamonds carry history, rarity, and value. When you work with natural diamonds, you’re holding something that has lived many lives - there’s a character you simply can’t replicate,” says Stephanie Gottlieb.

For many of their clients, the appeal is tied to meaning as much as aesthetics. “There’s a very emotional component to natural diamonds. Clients talk about wanting something ‘real,’ something they can pass down, something that carries the symbolism of commitment or celebration in a way that feels lasting.”

These designers sit firmly in the luxury tier and that positioning is part of the draw, particularly as clients become more value conscious. “Clients today are much more aware of the differences in long-term value, resale, and perception - and the declining price of lab grown diamonds. That awareness is pushing a lot of people back toward natural - especially for fine jewelry meant to last decades.” As Gottlieb notes, “Lab-grown hasn’t threatened our natural diamond business; if anything, it’s clarified our lane. It reaffirmed that we serve a client who values character, rarity, and emotional significance.” Greater transparency has strengthened trust, she says, with more time now spent helping clients understand value, longevity, environmental claims and the unique charm of natural stones.

By contrast, brands such as Brilliant Earth, VRAI and Kimaí build their proposition around transparency, ethics and accessibility. They appeal to younger customers who see the lab-grown option as the more ethical and responsible choice, avoiding mining concerns and associated environmental and human harm. But for this audience, price is the real unlock, since lab-grown are far more affordable than natural stones. According to a 2025 report, the reduced cost has led buyers to trade up, increasing average sizes from 1.31 to 2.45 carats between 2019 and 2025 and upgrading overall quality (13). “Lab-grown diamonds have certainly expanded access and offered an option for people who are drawn to size and sparkle at a lower price point. But I think of them as a different category entirely,” says Gottlieb. “Our clients see lab-grown as fun, trendy, or practical - great for fashion jewellery or for achieving a larger look without the investment.” These brands also lean on digital customisation tools, virtual try on's and streamlined online journeys that broaden their reach and make fine jewellery feel more democratic and accessible.

(The Price Gap: Mined vs Lab-Grown Pear-Cut Diamonds | in.Parallel Graphic)

(The Price Gap: Mined vs Lab-Grown Pear-Cut Diamonds | in.Parallel Graphic)

Some brands take a hybrid approach. Mejuri, for instance, recognises that lab-grown and natural stones can appeal to the same customer for different purposes, so they offer both. Diamonds are positioned as part of a contemporary wardrobe, where price becomes a feature rather than a barrier. Lab-grown stones make collecting, layering and updating jewellery not only stylistically possible but financially accessible.